Kyle Coertze, Investment Analyst at Cartesian Capital

We believe the market has grown overly optimistic in pricing in two additional rate cuts this year. While rate expectations, as implied by the FRA curve, is for a rate cut at the 29 May Monetary Policy Committee (MPC) meeting, we maintain that the first and potentially only cut this year will come at the 31 July meeting. This is conditional on April core inflation, due on the 21st of May, not materially surprising to the downside.

We believe the May meeting represents the last opportunity where the MPC can reasonably justify holding rates steady. Beyond that, the combination of a disinflationary trend and growing real policy restrictiveness is likely to compel action. We also expect the Committee to strike a more cautious tone thereafter – maintaining the policy rate at 7.25% beyond the September meeting, while leaving the door open to future adjustments should their QPM model point to a lower neutral rate.

Our rationale is as follows:

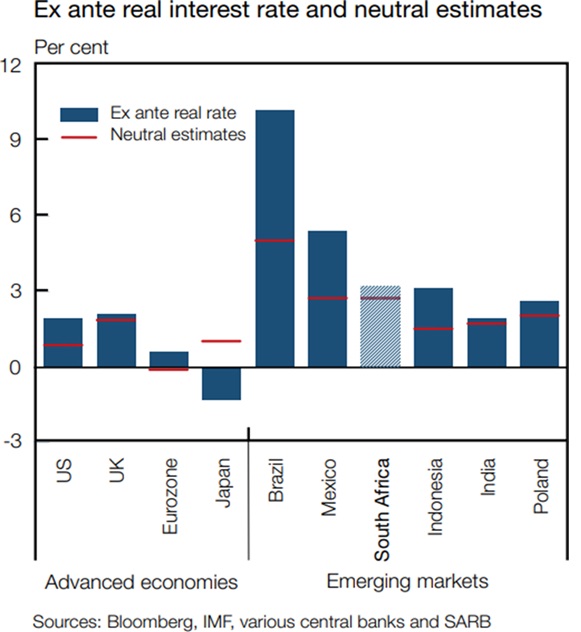

The South African Reserve Bank (SARB) has explicitly stated that it views the neutral repo rate as 25%.

This implies that only one additional rate cut would be required to reach this level.

The assumptions underpinning this estimate have since evolved. The proposed VAT hike has been reversed, and parties within the Government of National Unity (GNU) have agreed to pass Budget 3.0 when it is tabled on the 21st of May. These developments reduce the domestic equilibrium risk premium – which the SARB sees as the primary factor sustaining South Africa’s elevated policy rate (followed by the impact of G3 rates).

Scope for inflation target reform:

With core inflation having eased to 3.1% and edging closer to the lower bound of the 3–6% headline inflation target range, there is a growing case for revisiting the inflation SARB Governor Lesetja Kganyago has consistently advocated for a lower single- point target around 3%. The governor has argued that it would help anchor expectations more effectively and could be implemented with limited disruption – especially if supported by clear communication. While Finance Minister Enoch Godongwana has expressed caution, citing South Africa’s socio-economic vulnerabilities, a scenario in which inflation moves to or slightly below 3% and remains there could prompt a reassessment. If such a change can be made with little or no fiscal cost in the short to medium term, the Finance Minister may become more amenable to endorsing a lower target.

Upcoming Fed meetings and external risk assessment:

A July cut, as opposed to a May cut, would give the SARB additional time to factor in key external risks, such as the outcomes of the U.S. Federal Reserve meetings and developments in U.S. tariff policy. There are two remaining S. Federal Reserve meetings before the SARB announces its interest rate decision on the 31st of July.

Although the SARB will make its internal decision prior to the conclusion of the second Fed meeting – as is customary to allow time for the preparation of the Governor’s statement and other communication materials – the public announcement will be made after the Fed’s 30 July outcome. While the SARB will not have the benefit of the outcome of the Fed’s second meeting when finalising its decision, it will still be able to assess market expectations and consensus positioning leading up to that date. These market signals, along with any developments regarding U.S. tariff policy, will inform the SARB’s external risk assessment as it prepares to make its final decision.

Key data points to watch on 21 May

1. Budget 3.0 – The updated budget is expected to pass without much fanfare, but it’s still worth monitoring for any unexpected signals.

2. CPI Print – We expect April headline inflation to remain low, largely due to falling fuel prices. Core inflation is likely to ease gradually. While our base case is for a rate cut in July, a sharp downside surprise in core inflation could bring that cut forward to May, in our view.

In conclusion, while the SARB has ample justification to cut rates in May – given contained inflation, a narrower domestic equilibrium risk premium since March, and a still-restrictive real policy rate – we do not expect a cut at the May meeting.

Despite market pricing pointing to a May easing, we believe the Committee is more likely to wait until July, when it will have greater clarity on global trends and the inflation outlook.

That said, May is the final point at which the SARB can credibly delay cutting interest rates further. Beyond that, the risk of appearing behind the curve increases meaningfully.

ENDS